Whether you’re opening a new credit card, buying a new couch on credit, or applying for a new mortgage, the lender from whom you are borrowing will pull your credit score to see if you are a good borrower and how likely you are to pay the debt back on time (i.e., your creditworthiness). The interest that you will be paying on the loan is largely influenced by your credit score, which will impact the total amount that you have to pay back.

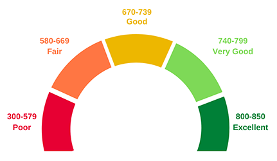

The most commonly used credit score is the FICO Score. The FICO Score was invented in 1989, and it has been the industry standard ever since. It ranges from 300 (poor) to 850 (excellent). When a lender pulls your credit, they are likely using your FICO Score. The interest rate they give you and the term of your loan largely depend on where you are situated in the ranges of scores below.*

Why your credit score matters

The primary reason why your credit score matters is because it affects the interest rate that you get on a loan. The higher your credit score, the higher your creditworthiness and the better interest rate the lender is willing to give you because they have less of a fear you will be defaulting on their loan. A lower interest rate means your monthly payment will be less, and consequently, the amount you have to pay back will be less. Having a lower interest rate, even just slightly, is most impactful on long-term loans, such as mortgages or auto loans.

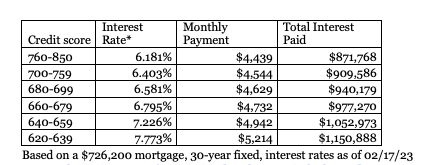

The table below looks at how different credit scores affect mortgage rates. As you can see, the higher the credit score, the lower the monthly payment and total interest paid. For example, by improving your credit score from 650 to 760, you could save $181,205 over the life of the mortgage.

*Source:https://www.myfico.com/credit-education/calculators/loan-savings-calculator/

What affects your credit score

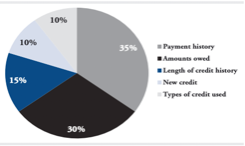

Credit scores are determined using five factors. The weight of each factor and how it impacts your credit score is shown in the pie chart below. As you can see, payment history and amounts owed (or credit utilization) make up 65% of your overall score.

Let’s break down each section:

- Payment history: The biggest factor that influences your credit score is whether you are making on-time payments. This means making on-time payments for mortgages, auto loans, and other installment loans, but also paying off your full credit card balance every month.

- Amounts owed/credit utilization: The credit utilization factor looks at how much credit you are using compared to how much credit you were given. For example, if your credit card limit is $10,000 and you have a balance of $5,000, your credit utilization is 50%.

- Length of credit history: The credit history factor looks at how long each of your credit lines have been opened and averages them out. For example, if you have a mortgage that you’ve been paying for several years, but you opened two new credit cards and a new auto loan in the last 12 months, your average credit history will be shorter.

- New credit: The new credit factor looks at how many new credit lines have been opened in a short period of time, as this represents a higher risk for lenders. Note that new credit inquiries (hard inquiries) also affect this factor regardless of whether you actually took out the credit or not.

- Types of credit used: Your FICO Score is also determined based on the different types of credit you use. In general, having multiple different types of credit (e.g., mortgage, auto loan, student loans, credit cards) improves a credit score.

Tips to improve your credit score

As a rule of thumb, you will want to focus on the areas that will have the biggest impact on your credit score.

- Make on-time payments: Accounting for 35% of your overall credit score, it’s really important that you make on-time payments and that you pay your full credit card balance every month. If you think you will forget to pay your credit card every month, make sure to set up automatic payments or schedule reminders.

- Check your credit reports for inaccuracies: It could be the case that you don’t even know that you are late on payments or that an account has gone into collection (e.g., unpaid medical bill). You may have moved or changed your email address, so the creditor has no way of reaching you. Make sure to check your free credit reports from the three major credit bureaus each year (Equifax, Experian, and Transunion) to see if there are any red flags. If you see inaccuracies, you can dispute them, and they can usually be removed from your credit report and improve your credit score within just a few months.

- Lower your credit utilization: FICO is looking to see a credit utilization of less than 30%. Going back to our example above, if you have a $10,000 limit on your credit card, you would want to try and keep your balance below $3,000 at all times. Reducing your credit utilization reduces your credit score (e.g., a reduction of 55% to 25% could reduce your credit score by as much as 75 points**). Increasing your credit limit (even if you don’t need it) is often a good way to lower your credit utilization below 30%.

- Avoid opening new credit before applying for a loan: Every time you open new credit (credit card, auto loan, refinancing student loans, furniture loan, etc.), the lender makes a hard inquiry into your credit history, which damages your credit score for up to one year. Opening new credit will also lower your average credit length history, which also damages your credit score.

As you can see, your credit score has nothing to do with how much money you make or how much your net worth is. Even if you are a high-income individual, it’s important to periodically review your credit score and credit reports to see if there is anything that is affecting it negatively, and if so, what steps you need to take to improve it. This is especially important if you plan on taking out a new loan, such as a mortgage.